FOR Communication 4/2023: High inflation in Poland is caused by the Monetary Policy Council

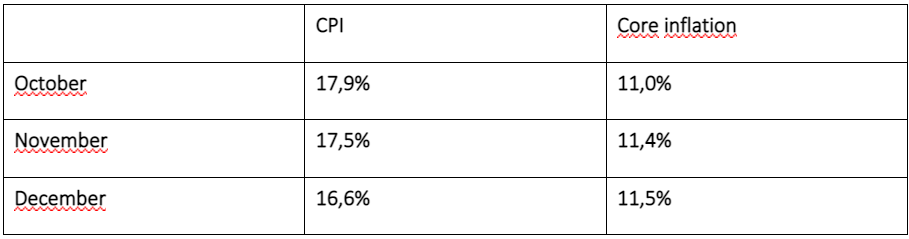

A slight decrease in inflation measured by the CPI (Consumer Price Index) at the end of 2022 should be treated with great caution because it is accompanied by an increase in core inflation, which is calculated by excluding food and energy prices from the market basket.

CPI and core inflation in Poland, Q4 2022

Source: GUS and NBP

CPI is the most widely known and used indicator by central banks as an measure in which the inflation target is expressed (in Poland it is 2.5%, plus or minus 1 p.p.).

Inflation, however, must also be looked at through the so-called core inflation, which is calculated excluding food and energy prices from the CPI. This is due to the fact that in the food industry and on the energy market there are often disturbances called "supply shocks", which mainly occur on global markets: increases or decreases in the prices of crude oil or wheat, sugar or coffee can significantly affect CPI changes in individual countries, although the internal demand pressure in the economies of these countries does not change. It may remain at a stable level, while the rising energy or food price on the global market raise the domestic CPI. Equally, falling energy and food prices in global markets may drive down the domestic CPI even as domestic demand pressure increase. Unlike the CPI, the core inflation index can be treated as free from the impact of external fluctuations. Core inflation more strongly than CPI reflects the impact of domestic factors, including domestic inflationary pressure.

CPI fluctuations resulting from sudden, unexpected price changes in global food and energy markets are not directly influenced by monetary policy, and this may justify a solution of simply waiting for the "supply shock" to wear off. The issue of reacting to changes in core inflation looks different: monetary policy is able to slow down its growth by raising the reference interest rate. And it should respond to a sufficiently deep decline in core inflation by lowering the rate. Such policy to be effective requires accurate prediction of core inflation determinants and adjusting the monetary policy response to these predictions (forward-looking approach), as well as an appropriate timing.

Core inflation in Poland in December 2022 was 11.5%, while the average in the European Union was 5.97%, and in the euro zone alone it was 5.2%. These huge differences in core inflation prove that the Polish monetary policy was pro-inflationary. These pro-inflationary mistakes had to be made mainly in 2020-2021.

The full content of the publication can be found in the file to download below.

Contact to author:

Prof. Dariusz Filar, economist, FOR external expert

[email protected]

Files to download